Page 87 - 95

P. 87

sion financing is therefore similar to limited-or non-

resource project finance, except that the revenues

are received under the terms of a concession agre-

ement. The project will be approached in a similar

way to limited-resource project financing in which

the risks are isolated and allocated to those most

qualified to bear them.

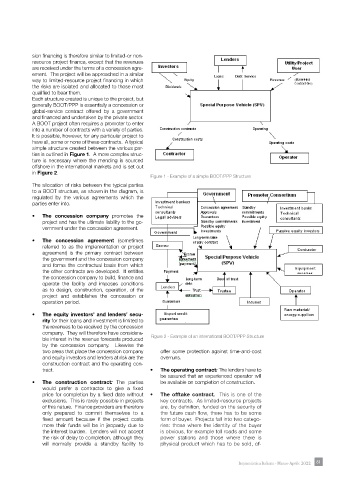

Each structure created is unique to the project, but

generally BOOT/PPP is essentially a concession or

global-service contract offered by a government

and financed and undertaken by the private sector.

A BOOT project often requires a promoter to enter

into a number of contracts with a variety of parties.

It is possible, however, for any particular project to

have all, some or none of these contracts. A typical

simple structure created between the various par-

ties is outlined in Figure 1. A more complex struc-

ture is necessary where the mending is sourced

offshore in the international markets and is set out

in Figure 2.

Figure 1 - Example of a simple BOOT/PPP Structure

The allocation of risks between the typical parties

to a BOOT structure, as shown in the diagram, is

regulated by the various agreements which the

parties enter into.

• The concession company promotes the

project and has the ultimate liability to the go-

vernment under the concession agreement.

• The concession agreement (sometimes

referred to as the implementation or project

agreement) is the primary contract between

the government and the concession company

and forms the contractual basis from which

the other contracts are developed. It entitles

the concession company to build, finance and

operate the facility and imposes conditions

as to design, construction, operation, of the

project and establishes the concession or

operation period.

• The equity investors’ and lenders’ secu-

rity for their loans and investment is limited to

the revenues to be received by the concession

company. They will therefore have considera-

ble interest in the revenue forecasts produced Figure 2 - Example of an international BOOT/PPP Structure

by the concession company. Likewise the

two areas that place the concession company offer some protection against time-and-cost

and equity investors and lenders at risk are the overruns.

construction contract and the operating con-

tract. • The operating contract: The lenders have to

be assured that an experienced operator will

• The construction contract: The parties be available on completion of construction.

would prefer a contractor to give a fixed

price for completion by a fixed date without • The offtake contract. This is one of the

exclusions. This is rarely possible in projects key contracts. As limited-resource projects

of this nature. Finance providers are therefore are, by definition, funded on the security of

only prepared to commit themselves to a the future cash flow, there has to be some

fixed amount because if the project costs form of buyer. Projects fall into two catego-

more their funds will be in jeopardy due to ries: those where the identity of the buyer

the interest burden. Lenders will not accept is obvious, for example toll roads and some

the risk of delay to completion, although they power stations and those where there is

will normally provide a standby facility to physical product which has to be sold, of-

Impiantistica Italiana - Marzo-Aprile 2022 81 81