Page 27 - 77

P. 27

as templates. In software, the unit cost is close to

nil. Adobe, for example, takes some financial risk in

releasing Creative Cloud for the price of a monthly

payment rather than the license fee of its compa-

rable on-site software. But it doesn’t have to ship

individual pieces of machinery that cost thousan-

ds, or millions, of dollars to produce—a greater risk

than sharing code. Revenue disruption at this scale

could lead to a more sustainable income stream,

but if anything were to go wrong the financial re-

sults could be devastating.

Still, given the potential that sellers and buyers see

in this pricing model, there’s a strong incentive to

make it work for all parties. In our work with com-

panies trying to get this right, three main obstacles

slow their progress:

• agreeing with customers on the value created

and how to share risk;

• managing the internal changes required to sup-

port a service pricing model; and

• “swallowing the fish”—planning for a disrupti-

ve period of rising costs and falling revenues,

before the financials find their new trajectory

When executive teams understand the risks and

opportunities of the equipment as a service (EaaS)

pricing model, they can develop offers that work for

buyers and sellers, limiting exposure and maximi-

zing the gains for both sides.

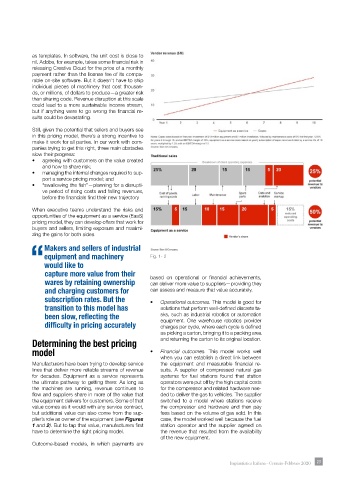

Makers and sellers of industrial

equipment and machinery Fig. 1- 2

“would like to

capture more value from their based on operational or financial achievements,

wares by retaining ownership can deliver more value to suppliers—providing they

and charging customers for can assess and measure that value accurately.

subscription rates. But the • Operational outcomes. This model is good for

transition to this model has solutions that perform well-defined discrete ta-

been slow, reflecting the sks, such as industrial robotics or automation

equipment. One warehouse robotics provider

difficulty in pricing accurately charges per cycle, where each cycle is defined

as picking a carton, bringing it to a packing area

Determining the best pricing and returning the carton to its original location.

model • Financial outcomes. This model works well

when you can establish a direct link between

Manufacturers have been trying to develop service the equipment and measurable financial re-

lines that deliver more reliable streams of revenue sults. A supplier of compressed natural gas

for decades. Equipment as a service represents systems for fuel stations found that station

the ultimate pathway to getting there: As long as operators were put off by the high capital costs

the machines are running, revenue continues to for the compressor and related hardware nee-

flow and suppliers share in more of the value that ded to deliver the gas to vehicles. The supplier

the equipment delivers for customers. Some of that switched to a model where stations receive

value comes as it would with any service contract, the compressor and hardware and then pay

but additional value can also come from the sup- fees based on the volume of gas sold. In this

plier’s role as owner of the equipment (see Figures case, the model worked well because the fuel

1 and 2). But to tap that value, manufacturers first station operator and the supplier agreed on

have to determine the right pricing model. the revenue that resulted from the availability

of the new equipment.

Outcome-based models, in which payments are

Impiantistica Italiana - Gennaio-Febbraio 2020 23